When you fill a prescription for high blood pressure or cholesterol, you might not think about why your copay is $5 instead of $50. But behind that simple number is a complex system designed by your health plan to save money-mostly by pushing you toward generic drugs. These aren’t second-rate medicines. They’re exact copies of brand-name drugs, approved by the FDA, and they cost 80-85% less. Health insurers and pharmacy benefit managers (PBMs) have spent decades building benefit designs that make generics the default choice. And it’s working-91.5% of all prescriptions filled in the U.S. in 2022 were generics, even though they made up just 22% of total drug spending.

How Insurance Plans Push You Toward Generics

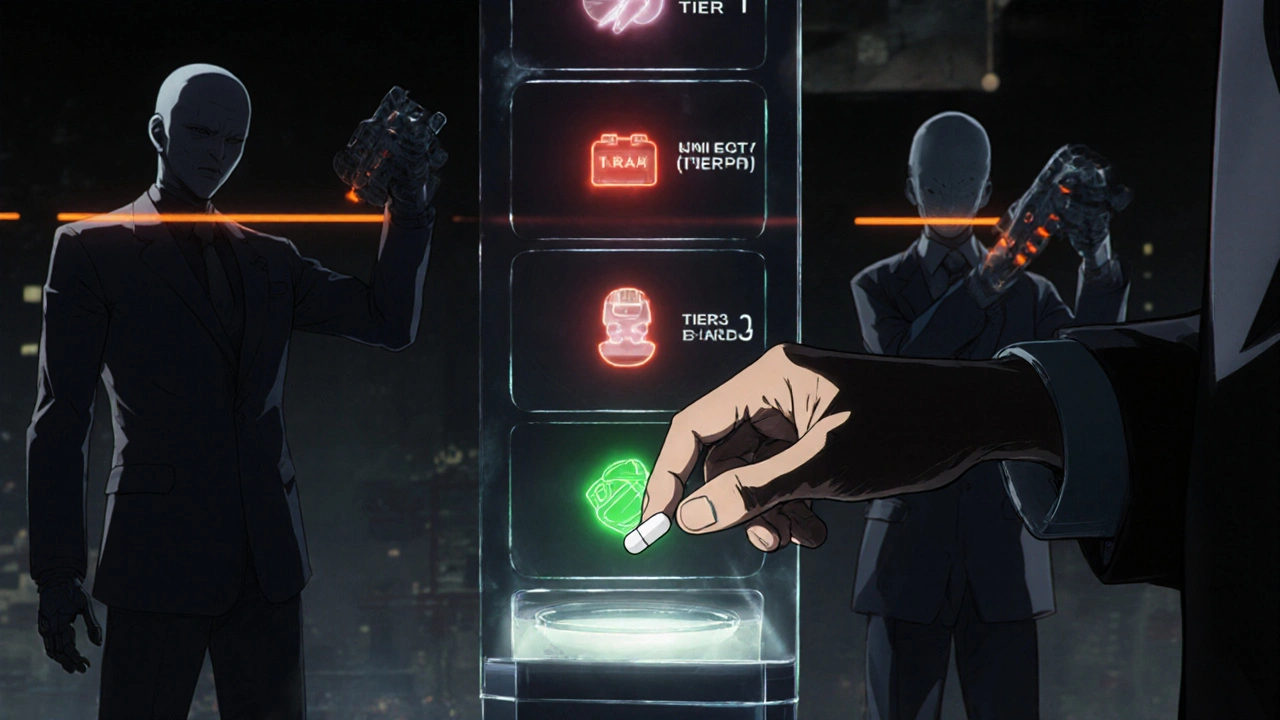

Most health plans don’t just encourage generics-they engineer their benefits to make them the only smart choice. The main tool? Tiered formularies. Think of it like a pricing ladder. At the bottom is Tier 1: generics. You might pay $0 to $10 for a 30-day supply. Tier 2 is preferred brand-name drugs-maybe $25 to $50. Tier 3? Non-preferred brands, often $60 or more. If your plan doesn’t cover your brand-name drug at all unless you’ve tried the generic first, that’s called step therapy. And it’s used in 92% of Medicare Part D plans. Some plans go even further. Closed formularies block brand-name drugs entirely if a generic exists. One Medicare HMO study found this approach cut brand-name use by nearly 29%. And in 49 states, pharmacists can swap a brand for a generic without asking your doctor-thanks to mandatory substitution laws. You might not even know it happened.The Real Savings-And Who Gets Them

The numbers are staggering. Between 2013 and 2022, generic drugs saved the U.S. healthcare system over $3.7 trillion. That’s more than $370 billion a year. For patients, that means a $150 brand-name drug might cost just $25 as a generic. But here’s the catch: you’re not always seeing the full savings. Pharmacy benefit managers (PBMs)-the middlemen between insurers, pharmacies, and drugmakers-often use a practice called spread pricing. They tell your plan they’re paying $10 for a generic, but actually pay the pharmacy $7. You pay your $10 copay. The $3 difference? That’s profit for the PBM. A 2022 USC Schaeffer Center study found patients were overpaying by $10-$15 per prescription because of this. Even worse, some plans charge you a copay that’s higher than the actual cost of the drug. Then they take back the difference-called a copay clawback. You walk away thinking you paid $15 for a $5 drug. The plan pockets the rest.How Different Plans Compare

Not all health plans treat generics the same way. Medicare Part D, which covers over 50 million seniors, uses standardized tiers but varies widely by plan. In 2024, generic copays ranged from $0 to $15. Medicaid, which covers low-income Americans, actually has a higher generic dispensing rate-89.3%-than commercial insurance at 87.1%. That’s because Medicaid is tightly regulated. States can only reimburse pharmacies up to 250% of the average manufacturer price (AMP), forcing pharmacies to use generics to stay profitable. Self-insured employers-companies that pay for their own employees’ health care instead of buying insurance-are especially aggressive. A Johns Hopkins study found two large employers saved 9-15% on drug costs just by switching patients to cheaper, therapeutically equivalent generics. No drop in effectiveness. Just lower bills. Then there’s the new kid on the block: Mark Cuban Cost Plus Drug Company. Launched in 2022, it sells generics directly to consumers without insurance middlemen. A 2023 analysis found patients saved a median of $4.96 per prescription. But here’s the twist: Medicaid patients didn’t save a cent. Why? Because Medicaid already pays the lowest possible price. The savings were only for people paying out-of-pocket.

What Patients Really Experience

On Reddit, one user wrote: “Generic copay went from $5 to $0 last month-anyone else?” Over 87% of the 142 replies said yes, and they were thrilled. But another thread on Patients Like Me told a different story: “I paid $22 for a generic that I thought should’ve been $8.” That’s the copay clawback again. A Kaiser Family Foundation survey found 68% of Medicare beneficiaries were satisfied with their generic coverage. But 22% struggled to get their doctor to appeal when a brand-name drug was denied. And 14% had to go through multiple appeals. Then there’s the clinical side: 31% of doctors reported patients had side effects after being switched to a generic. Not because the drug was bad-but because some patients react differently to fillers or coatings, even if the active ingredient is identical.Who Controls the System-and Why It’s Broken

Three PBMs-CVS Caremark, OptumRx, and Express Scripts-handle 83% of all prescription claims. They build the formularies, negotiate rebates, and set copays. Their profits come from the gap between what they charge insurers and what they pay pharmacies. That’s why they don’t want transparency. In 2023, PBMs secured $195 billion in rebates and discounts for health plans. But most of that money never reached patients. The Department of Labor is finally pushing back. Starting January 1, 2025, all Explanation of Benefits (EOB) statements must show exactly how much the drug cost, how much the PBM paid, and how much you paid. No more hiding. If your copay is $15 and the drug cost $8, you’ll see it.

The Future: More Rules, More Transparency

The Inflation Reduction Act, which took full effect in 2025, capped out-of-pocket drug costs for Medicare Part D at $2,000 a year. That’s huge. It means seniors will no longer ration pills to save money. But it also changes how insurers think about generics. If your costs are capped, the incentive to push cheaper drugs shrinks. Plans may start shifting focus to other cost controls. In 2026, CMS is launching the GENEROUS Model for Medicaid. It’s designed to negotiate lower generic prices directly with manufacturers and standardize coverage across states. Projections say it could save $40 billion over ten years. Meanwhile, the generic drug market itself is consolidating. Teva, Viatris, and Hikma control nearly 38% of the market. That reduces competition-which can drive prices back up. The USC Schaeffer Center warns: without more competition among generic makers, savings won’t last.What You Can Do

You don’t have to be a passive player in this system. Here’s how to take control:- Always ask: “Is there a generic version?” Even if your plan says yes, your doctor might not have checked.

- Check your EOB after January 2025. If your copay is higher than the drug’s actual cost, contact your plan.

- If you’re switched to a generic and feel worse, tell your doctor immediately. You have the right to appeal.

- Compare prices. Sometimes, paying cash at a pharmacy like Walmart or Costco is cheaper than using your insurance.

- Use tools like GoodRx or the Mark Cuban Cost Plus Drug Company to see what a drug really costs outside the insurance system.

Generics Work-But the System Needs Fixing

Generic drugs are one of the most successful cost-saving tools in modern healthcare. They’re safe, effective, and affordable. But the system designed to deliver those savings is broken. PBMs, insurers, and pharmacies all benefit-sometimes at your expense. The answer isn’t to stop using generics. It’s to demand transparency. To know what you’re really paying. And to push back when the math doesn’t add up.The goal isn’t just lower costs-it’s fair costs. And that starts with you asking questions.

9 Comments

Paige Lund

So let me get this straight-we’re supposed to be thrilled that we’re paying $0 for a pill that someone else made $3 off of? Classic.

Derron Vanderpoel

I just got switched to a generic for my blood pressure med last month and I swear I felt like a zombie for two weeks. My doctor said it was 'just the placebo effect'-but I know my body. I asked for the brand back and they made me jump through five hoops. I’m not crazy, I just want to not feel like I’m slowly turning into a ghost.

Timothy Reed

It's important to recognize that while the PBM system is deeply flawed, the widespread adoption of generics has prevented millions of Americans from choosing between medication and groceries. The real issue isn't generics-it's the lack of transparency and the extraction of profits by intermediaries who add no clinical value. Reform is coming, but we need to protect the gains while fixing the exploitation.

Codie Wagers

Generics are not 'exact copies'-they are chemically equivalent, yes, but the excipients, fillers, binders, and coatings vary. These are not inert. They alter dissolution rates, bioavailability, and, yes, sometimes patient tolerance. To claim otherwise is not science-it’s corporate propaganda masquerading as public health. The FDA approves them for 'bioequivalence'-not 'identity'. There is a chasm between those two concepts, and patients are the ones falling into it.

And don’t get me started on the moral bankruptcy of a system where a $5 drug costs you $15 because the PBM pocketed the difference. You're not saving money-you're being robbed with a smile and a formulary chart.

Meanwhile, the same people who push generics as 'cost-effective' refuse to cap PBM profits or mandate rebate pass-throughs. Why? Because they’re the same entities profiting from the game. It’s not capitalism-it’s predation dressed in white coats.

The Inflation Reduction Act’s $2,000 cap? A Band-Aid on a severed artery. It doesn’t touch the root: PBMs control the supply chain, the pricing, the formularies, and the data. They’re the unregulated oligarchs of pharmacy.

And now we’re supposed to trust the 'transparency' of EOBs in 2025? Please. If you think a 10-line disclosure on a PDF will undo decades of systemic theft, you’ve never read a Terms of Service agreement.

Real reform? Ban spread pricing. Mandate direct manufacturer-to-pharmacy pricing. Eliminate PBMs as middlemen. Let pharmacies bill insurers directly. And stop pretending that 'affordable' means 'exploitative'.

Until then, yes-take the generic. But know this: you’re not getting a bargain. You’re getting the scraps from a table where the rich ate first.

Angela Gutschwager

My copay went from $5 to $0 too 😊

Dion Hetemi

Let’s be real-91.5% generic usage isn’t a win, it’s a surrender. We’ve normalized being herded into cheap meds like cattle. The fact that Medicaid has a higher rate than commercial insurance? That’s not efficiency-that’s poverty enforcement. And the 'savings' are illusions. The system isn’t saving money-it’s shifting costs onto patients, pharmacists, and doctors while PBMs rake in billions. This isn’t healthcare innovation. It’s financial engineering on the backs of the sick.

And don’t even get me started on the 31% of patients who have side effects after switching. They’re told to 'tough it out' while their doctor gets a bonus for hitting 'generic utilization targets'. We’re not treating patients-we’re optimizing spreadsheets.

Mark Cuban’s model? Cute. But it only works for people who can pay cash. For everyone else? Still stuck in the same rigged game. The system doesn’t need tweaks-it needs a demolition crew.

Kara Binning

Let me be perfectly clear: America is the only country in the world where a life-saving generic costs more than a latte because of corporate greed. We have the technology, the science, and the moral capacity to fix this-but we don’t have the will. Why? Because the people who profit from this mess vote, donate, and own the politicians. This isn’t about healthcare. It’s about power. And until we treat pharmacy benefit managers like the cartel they are, we’re all just paying for the privilege of being exploited.

And yes-I’m angry. You should be too.

Zac Gray

It’s fascinating how the same people who scream about 'big pharma' never mention the PBMs-the real puppet masters. They’re not drugmakers, they’re financial firms with pharmacy licenses. They don’t produce anything. They just move money around and call it 'negotiation'. And we let them because we’re too busy being grateful for $0 copays to ask who’s really pocketing the difference.

My cousin took a generic for her thyroid and her TSH went haywire. She had to go through three appeals just to get her old brand back. The doctor said, 'It’s the same thing.' But biology doesn’t care about FDA equivalency charts. It cares about how your body reacts. And the system doesn’t care about her.

Transparency is a start. But what we need is accountability. PBMs shouldn’t be allowed to profit from the gap between what they charge and what they pay. Period. If they want to make money, they should do it by reducing waste, not by inflating copays.

And if you’re paying $15 for a $5 drug? You’re not getting a deal. You’re being scammed. And the fact that this is legal? That’s the real scandal.

Reema Al-Zaheri

While the systemic issues surrounding pharmacy benefit managers are indeed profound, it remains empirically accurate that generic medications have, since their widespread adoption, substantially reduced the financial burden on both individual patients and the broader healthcare infrastructure. The 91.5% utilization rate is not an artifact of coercion, but rather a reflection of clinical equivalence, regulatory rigor, and economic rationality. The problem lies not in the use of generics, but in the opacity of pricing mechanisms, the absence of rebate pass-throughs, and the structural misalignment of incentives within the supply chain. Until these structural inefficiencies are addressed-through legislative intervention, competitive market mechanisms, and mandatory disclosure-the benefits of generics will continue to be disproportionately captured by intermediaries, rather than redistributed to patients. The solution is not to abandon generics, but to reform the architecture that governs their distribution.